Annex Bulletin 2006-34 September 12, 2006

An OPEN client edition

INDUSTRY TRENDS

Updated 9/12/06, 7:00PM PDT

Analysis of Stock Buyback Trends...

A Fading Fad

Dell, Erstwhile "King of Fluff," Suspends Stock Buybacks

SCOTTSDALE, Sep 12 - The erstwhile "King of Fluff" has lost its crown. Or more accurately, it has tossed its crown. Buried inside the 9/11 Dell press release about an expanding SEC investigation into its accounting practices, was the news that the company was suspending its multi-billion dollar stock buyback program.

The buyback news got virtually no play in the subsequent media stories. Nada. Never mind that Dell had spent about $28 billion repurchasing its shares. Nobody seem to care about that anymore. Like death and suffering in the Middle East, the stock buybacks have become banal. Taken for granted. A shrug. Such indifference suggests the passing of an era and a beginning of the end of a fading fad.

But what a fad it has been, almost a trend, certainly by its longevity, except for its top-down initiation...

The "King of Fluff"

Back in October 1998, we crowned Dell the "King of Fluff." And we called the stock buybacks "the latest Wall Street fad: the expensive (multi-billion) corporate 'cabbage patch' dolls of the 1990s - the stock buybacks." Here's an excerpt from that Annex Bulletin...

"As John Naisbitt noted in his 1980s bestseller book, "Megatrends," "fads are top down; trends are bottom up." As a result, fads tend to burn out like a flash in a pan; trends burn brightly for a long time.

During the last three years alone, corporate America has spent nearly half a trillion dollars on Wall Street's virtual "cabbage patch" dolls - without creating a single new job or a product. Stock buybacks attracted more money in 1990-1997 than did the economies of all developing countries in the world - combined! (about $550 billion, according to a United Nations report - see Annex Bulletin 97-38, 10/16/97).

(An excerpt from "Corporate 'Cabbage Patch' Dolls of the 1990s," 1998)

And is that good? No way, we said back in October 1998, echoing our exchange with the former IBM chairman and CEO at the 1997 annual meeting in Dallas (see "Stock Buybacks Questioned," Apr 1997). And here's why not...

Bloomberg News Wire: "An Illusion of Prosperity."

"It's a waste of capital - it doesn't create a single product or a single job," this writer was quoted as saying in the Bloomberg News Oct 27 story. "'It creates an illusion of prosperity by boosting the financial results without adding a cent to the bottom line,' Djurdjevic said."

The New York Times: "A Wall Street Perversion."

"But Bob Djurdjevic, president of Annex Research, called the repurchase a 'Wall Street perversion,' that benefits selling institutions to society's detriment, and artificially inflates current earnings and growth," the Times said. "IBM has already spent several small countries' GDPs on share repurchases - $23 billion and counting - without creating a single product or a single job," he said. "It's a signal they don't have the imagination or creativity to employ the capital more productively."

Dow Jones Newswires: "Paying Off Wall Street."

The Dow Jones wire quoted "the publisher of the Annex Bulletin in Phoenix as saying that the program "demonstrates a lack of creativity." "They're saying they can't think of a better way to invest in the (technology) industry," Djurdjevic said, adding that he is opposed to stock buybacks in general. "Instead they are paying off Wall Street (in exchange for) good opinions of IBM's stock."

Since that time, the 1998 "fad" has become a pervasive Wall Street trend. Led by IBM, Microsoft and Intel, the top 10 IT companies (in terms of market cap) have spent about $269 billion on stock buybacks since the time our above report was published. Just to put things in perspective, that's like the GDP of Austria.

That's also nearly three times as much money as the amount by which their aggregate shareholders' equity increased during the same time ($97 billion). Yet despite such a massive redistribution of wealth, far greater than the dividends have ever been, the amount of "fluff" in the market capitalization of the top 10 companies has been vastly reduced (by about 62% since 1998).

"Fluff?" That's what we called the market cap-over-equity ratio back in 1998. In other words, the amount of Wall Street goodwill or affection for in a stock price. Unlike equity, however, which is "money in the bank," goodwill can be here today and gone tomorrow. And although the market cap of the top 10 companies has remained remarkably stable in the last eight years (at about $800 billion), the amount of fluff in it has dropped from 86% of the total market cap to 69% now. And the average "fluff ratio" has fallen from 12.5 to 4.7 (times equity) since 1998.

In other words, there is a lot more substance and less "fluff" in today's valuation of the top IT leaders than there was eight years ago. That's because the companies engaging in share repurchases are no longer getting the bang for the buck (in terms of their stock price boost) they used to in the early years of the trend (see the above chart).

No wonder companies like Dell now, and Sun Microsystems (in fiscal 2005), for example, are suspending this practice while others are scaling down. Still, there are IT vendors, such as Microsoft, Intel, IBM and HP, that have actually increased their stock buybacks in the last two years. Each to his own, we suppose.

Diversity of views is especially obvious in the case of Accenture, for example. This IT services leaders has proven that you can achieve a stellar stock market performance without having to placate Wall Street institutions with billions of dollars. The company has largely abstained from the stock buyback craze, preferring to grow its business and its market cap the old fashioned way - by making money, rather than giving it away. Yet its stock appreciation leaves most of its rivals in the dust (see the chart).

So how would have these IT companies done had they not fallen for the stock buybacks scheme? Adding the share repurchases back into equity provides an interesting perspective into their real Wall Street marketing prowess. Microsoft and Oracle come out on top, with a 2.5 "market cap-over-equity plus stock buybacks" ratio. IBM is dead last. And EDS, Intel and Dell are just a little above Big Blue.

So therein may lie another indication of why IBM stock has been languishing relative to competition, despite the company's solid actual financial results. It has failed to sell its vision of the future to Wall Street despite greasing it with billions of dollars in share repurchases.

Are Buybacks Bad?

So are stock buybacks bad for shareholders? They are for some, not all. Most of all, they are bad for business. Why? Because they deprive the company of potential sources of future growth, indigenously or by acquisitions.

But Wall Street loves them (of course, since it invented them). Besides being the main recipient of the hundreds of billions of dollars, institutional investors can also benefit from capital gains, and by getting to make the investment decisions the management of the company should be making with IBM's and other stock buyback participants' money.

Meanwhile, all general (smaller) shareholders have to show for in return for $73 billion their company (IBM) has spread around Wall Street is a depressed stock price. And a loss of control over how their hard-earned dollars get reinvested. Some of that money could have ended up propping up the Argentina bankruptcy, for instance, or the Iraq and Afghanistan wars, or funding some other lost cause or harebrained ideas of how to build a better mousetrap.

So what should Big Blue (and others) have done with the $73 billion (or $269 billion)? Reinvested it in business, of course. That's how smart managers, such as those who run Accenture, for example, do things. By innovating and buying imaginative start-ups. As we said back in 1998...

"They could have picked up the Yellow Pages and randomly bought thousands of IT companies for $23 billion," [make that $73 billion now]. I said [back in 1998]. "Chances are, even using such a shotgun method, one might have ended up with the next 'Netscape' or a 'Yahoo' in my business portfolio." Or a Google.

Third, I'd set aside a portion of the money for a "Save the Seals"-type fund. Its proceeds would be used to protect the fledgling, but creative, IT entrepreneurs from being clubbed to death by the industry's juggernauts, such as Microsoft, for example, before the young pups have a chance to grow up.

Instead, the IBM shareholders have lost $23 billion of real assets in return for $120 billion of "fluff," the here today, gone tomorrow stock market paper gains.

As we now know, "tomorrow" is here today. And the "fluff" that billions of stock buyback dollars injected in the stock is now long gone. Big Blue's "fluff ratio" is down 51% since 1998. Microsoft's "fluff ratio" is down 58%; Intel's down 46%; Dell's down 70%; Sun's down 56%, etc. (see Table 1 for more details). See what we meant?

Winners and Losers

Every scheme has its winners and the losers. Winners are obviously Wall Street institutions. But who are the losers? Let's go back to the SUMMARY of our 1998 report for an answer to that question...

So what does that tell us? That the Wall Street casino is for suckers?

If so, what else is new? Most sensible people would have figured that out for themselves by now. Isn't the Las Vegas casino for suckers, too? The only difference is in the dress code. One is stylish and pin-striped; the other garish and loud.

But they both have one thing in common: The suckers. The "Mr. and Mrs. Middle America;" the "get-rich-quick" "Archie Bunkers" of the 1970s, who keep filling the casino owners' pockets as if there were no tomorrow. And they may eventually get their wish (of "no tomorrow") when the Babyboomers start cashing their retirement checks, only to find that there is only greed in their accounts.

No investment fads are possible without the government collaboration, active or passive. Active, because the lowering of the capital gains tax in the 1990s made the buybacks a preferred way of returning capital to (some) shareholders to the dividends (that reach all). Passive, because the feds could have taken action to stop it but did not.

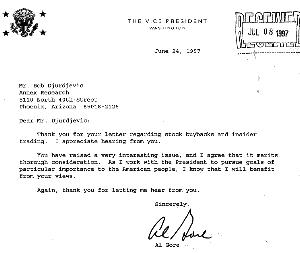

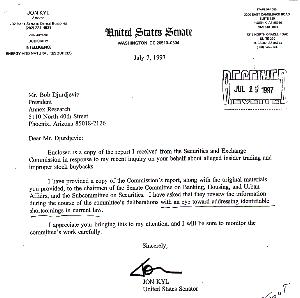

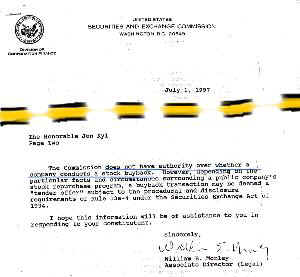

Here's a 2002 account of our July 1997 correspondence with several senior White House and Senate and SEC officials:

We�ve been writing about it ever since 1996, for example. We even exchanged correspondence back in July 1997 with vice president Al Gore, some U.S. senators, and the SEC. We thought it was a conflict of interest if officers sell their shares at the same time they are directing the company to buy back huge amounts of stock. That�s like selling deflated shares to yourself at market prices!

Vice President Gore thought we'd raised "an very interesting issue" that "merits thorough consideration." Senator Jon Kyl said he'd forwarded the information to the chairman of Senate's Banking, Housing and Urban Affairs and the Subcommittee on Securities, for "deliberations with an eye toward addressing identifiable shortcomings in current law." The SEC said it didn't have the jurisdiction over stock buybacks.

Yet our warnings have fallen on deaf ears. Which is proof positive that the unsavory actions that Gerstner, Lay, Skilling et. al. took are only symptoms of a larger problem. A macro view of these scandals shows that political plutocracy has replaced the once free and democratic America.

None of these scams or corporate abuses of power would have been possible had the government and/or the media done their job diligently and vigilantly.

�Silence is acquiescence,� goes an old saw. By remaining silent and passive, if not outright supportive of Gerstner, Lay, Skilling et. al., despite warnings about their self-dealings, the government and the media should bear their share of the responsibility.

(An excerpt from "Insider Trading....", Apr 2002)

{kind=link}

{kind=link}

{kind=link}

Then there is a matter of insider trading. Martha Stewart became a beacon of government's righteousness as she was trotted off to jail for having lied about trading a stock based on an insider tip.

Stock buybacks are the flip side of that situation. No one can have better inside information about the company than the insiders who run it. Yet they are allowed to make major stock buy decisions on behalf of the company to the tune of billions of dollars that ultimately influence the price of the stock. No outsider has access to such information. And then they can also exercise their options, thus profiting from the sale of the discounted shares while the company they run is buying them.

And that's legal and fair?

Contrast such government inertia to the zeal with which authorities pounced on HP over its boardroom scandal in the last two days. Some Representatives are even calling for new legislation. Meaning, some big toes have been stepped on.

No such vigilance was in evidence when it came to stock buybacks. Too many powerful interests are being served by them. As for the small shareholders... oh well. They did not have to play, did they? And so life goes on...

Row, row, row your boat

Gently down the stream.

Merrily, merrily, merrily, merrily,

Life is but a dream.

...for some on Wall Street, anyway.

Meanwhile, better hang on to your wallet while rowing down the stream, if you're a small investor.

|

Annex Clients CLICK HERE to view a detailed table |

Happy bargain hunting!

Bob Djurdjevic

![]() Click

here for PDF (print) version

Click

here for PDF (print) version

For additional Annex Research reports, check out... Annex

Bulletin Index 2006 (including all prior years' indexes)![]()

![]()

Or just click on  and use "company or topic name" keywords.

and use "company or topic name" keywords.

Volume XXII, Annex Newsflash 2006-34 Bob Djurdjevic, Editor 8183 E Mountain Spring Rd, Scottsdale, Arizona 85255 The copyright-protected information contained in the ANNEX BULLETINS and ANNEX NEWSFLASHES is part of the Comprehensive Market Service (CMS). It is intended for the exclusive use by those who have contracted for the entire CMS service. |

![]()

Home | Headlines | Annex Bulletins | Index 2006 | About Founder | Search | Feedback | Clips | Activism | Client quotes | Workshop | Columns | Subscribe