Annex Bulletin 2005-16 May 25, 2005

Confidential

Client Edition

IT SERVICES

Analysis

of CSC’s Fiscal Fourth Quarter and Full Year 2005 Results

Harvesting Records

Strong Results During Calendar First Quarter, Especially in Europe

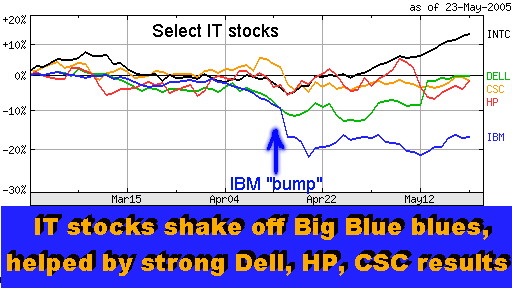

PHOENIX, May 25 – What European slump? Computer Sciences Corp.’s (CSC) fourth quarter of fiscal 2005 results, ended March 31, should dispel any doubts that IBM’s problems in Europe were pervasive.

CSC European revenues were up 19% (up 14% in constant currency) to $1.3 billion, a new record. The new business awards from the Old Continent contributed to record new signings (from continuing operations) in the fourth quarter and the full year. And all that happened during the calendar first quarter of 2005, which was supposed to be weak, based on IBM’s results (see “Slammed and Dunked,” Apr 2005).

CSC’s

worldwide net earnings in the latest quarter soared to $412 million, or

$2.13 a share, from $191 million, or $1.01 a share, a year ago.

The company’s bottom-line figure was boosted by a one-time net gain

of $230 million, or $1.19 a share, related to its sale of some of its

DynCorp business units (see “Gearing

Down on Purpose, Feb 2005).

CSC also booked a special charge of $18.4 million, or 10 cents a share after

taxes related to its redemption of $1 billion worth of debt, reducing its

debt-to-equity ratio to an enviable 18%.

Revenue

from continuing operations increased to $3.9 billion in the period that

ended on Mar 31, up from $3.6 billion a year ago.

CSC’s income from continuing operations, excluding special items, came in at 96 cents a share, while its profit from total operations was $1.04 a share. On average, Wall Street was expecting EPS of $1.07 on revenue of $3.77 billion, according to a Thomson First Call survey.

No

wonder CSC’s shares rose over two points in evening trading, after surging

more than three points on Tuesday (May 24).

For the last six months, however, they are down about 21%, since

reaching the 12-month high of $58 in December.

And CSC’s overnight gains also fizzled.

The stock was trading early morning today just a shade above its

yesterday’s price of $45.78 (see the charts).

Full Year Results

For the full year, CSC reported revenues from continuing operations of just over $14 billion, up 5% from a year ago total. The main reason for a (mere) single digit growth were the divestitures of two DynCorp units (see “Gearing Down on Purpose, Feb 2005). But the sale dropped $314 million to CSC’s bottom line, boosting its total net earnings for the year to $810 million, up 56% from a year ago.

CSC also continued its strong sales performance closing $2.7 billion of new business in the fourth quarter. This lifted the full year’s new contract awards to $16.8 billion, $16 billion of which came from continuing operations.

“We

are pleased with our performance for the fourth quarter and the year,”

said CSC’s CEO Van Honeycutt in a statement. “Given the re-profiling of

our U.S. federal government business due to the divestiture, the redemption

of term debt and strong major business awards, we have enhanced our

competitive position and financial flexibility.”

The

“re-profiling” resulted in a 6% drop in federal government business in

FY05. But Honeycutt said the

pipeline of future opportunities in this market is up 31% from a year ago to

$33 billion. “And we intend

to win our fair share of that,” he added. Indeed, the company has already won $820 million in awards in

FY06 to-date (meaning in the last six weeks).

In the commercial market, which represents two-thirds of CSC’s business, the company reported double-digit (11%) growth in FY05 to $9.4 billion. As you saw from the opening paragraphs, the European market was particularly strong, rising 18% for the year. With revenues of $4.3 billion, CSC Europe is now considerably bigger than its $3.8 billion U.S. commercial market.

Given

IBM’s recent problems in Europe, especially in the services area, and Big

Blue CEO’s comments that the company would become more aggressive, CSC

executives were quizzed about whether or not they saw that being reflected

in price-cutting.

Not

so, replied Honeycutt. “We

see a lot of activity from them (IBM), but we don’t see irresponsible

bidding.” He added that the

pricing has generally stabilized. And

that’s good news for both CSC and other IT services vendors’

shareholders.

“We’re mindful of the consolidating IT market,” said Honeycutt. “But we don’t see anybody reckless bidding or trying to buy in.”

Strong Balance Sheet – Hint of

Acquisitions

The

redemption of $1 billion of debt to which the CSC CEO referred above cost

the company $18.4 million in after-tax charges in the latest period, but it

also significantly enhanced its balance sheet.

The debt-to-total capitalization ratio improved from 30% last year,

to 17.6% in the latest period, boasted Leon Level, the CSC’s CFO.

The

company also set a record annual free cash flow of $475 million.

So

stand by for CSC to put some of the money it saved and it made to work.

“Given the strength of our balance sheet, maybe we’ll enter some

market we’re not in yet, probably through acquisition,” hinted Honeycutt

in the post-release teleconference with analysts.

He was not any more specific as to what type of an acquisition he had

in mind.

Asked

about what the best uses of its accumulating capital would be, the CSC CEO

replied as if he were with Annex Research.

“If

we can invest that cash in some spectacular acquisition, with great revenue

and profit growth - that’s the best use of our cash,” Honeycutt said.

“Second to that would be securing new large transactions; and third

would be lowering the share base” (i.e., stock buybacks).

It’s

refreshing to see that there are some CEOs around who seem immune to the

Wall Street stock buyback hype. Honeycutt

evidently believes that minding the store (investing in operations) is more

important than greasing Wall Street palms.

Summary & Outlook

During

the fiscal year 2005, CSC faced a number of challenges, both internal and

external. Internally, the company digested its 2003 DynCorp acquisition

and sold off

some of its parts.

Externally, the company faced soft demand for professional services,

and a temporary reduction in federal government spending on projects that

represent CSC’s sweet spots.

“Despite these challenges, we delivered record revenues, record earnings per share, record new business awards, record free cash flow, and a balance sheet that afford, for all practical purposes, unlimited flexibility,” said Level, the company’s CFO. He had good reasons to be boastful. For, it is in hard times that management’s mettle is tested.

So what can we expect in fiscal year 2006?

Honeycutt

predicted the company’s fiscal 2006 profit would range between $3.20 and

$3.30 a share. The CEO pegged revenue for the year at between $15 billion and

$15.2 billion, up 7% to 8% over the fiscal year 2005 total.

Those are modest goals. They certainly seem easily achievable under the current market conditions. Looks like CSC is setting the bar intentionally low so it could harvest a new crop of records a year from now. Which is not a bad policy given that the company is not trying to buy favors on Wall Street through stock buybacks.

Happy

bargain hunting!

Bob Djurdjevic

![]()

For additional Annex Research reports, check out...

2005 IT: CSC: Harvesting Records (May 2005); IBM Trumps Trump (May 2005); Tweaking Big Blue (May 2005); Dell Rings the Bell (May 2005); Stock Buybacks: The Phantom Is Back (May 2005); EDS Misfiring on All Cylinders (May 2005); HP Surges, Dell Slumps; Lenovo Completes IBM Deal (May 2005); Capgemini Jettisons Healthcare in N.A. (Apr 2005); HP: From India to Poland (Apr 2005); IBM: Slammed and Dunked (Apr 2005); Accenture: Roaring Ahead (Apr 2005); Fujitsu Unveils New Servers (Mar 2005); EDS Executive Suite; HP's New CEO (Mar 2005); An iSeries Revival (Mar 2005); EDS Booster Club Fees Rise (Mar 2005); An Upside-Down View (Mar 2005); The Worst of Both Worlds (Mar 2005); Octathlon 2005: Accenture Wins (Mar 2005); IBM Global Services: Smaller, Shorter - Better? (Mar 2005); IBM 5-yr Forecast: Quality over Quantity (Mar 2005); Rumor Lifts EDS', Fujitsu's Shares (Mar 2005); Capgemini: Turning the Corner (Feb 2005); IBM Servers to Grow Again (Feb 2005); Carly's Fickle Fans (Feb 2005); CSC: Gearing Down on Purpose (Feb 2005); EDS: Grossly Overpriced Stock (Feb 2005); IBM Historical Update: 2004 Shot in the Arm (Feb 2005); New HeadTurners Series #1 (Feb 2005); IBM: A Crescendo Finale! (Jan 2005); Accenture: Strong Finish, Better Start (Jan 2005); Annex Coverage 2004: IT Services Dominate (Jan 2005)

2004 IT: EDS: The Titanium Stock (and other Wall Street tales) (Dec 2004); IBM PC: Good Riddance (Dec 2004); Fujitsu: Recovery Continues (Nov 2004); IBM Server Renaissance (Nov 2004); HP Hits Home Run (Nov 2004); Capgemini: Revenue, Stock Soars (Nov 2004); EDS: Jordan's Swan Song? (Nov 2004); To Russia with Love and $ (Oct 2004); IBM: Slow Quarter No Longer (Oct 2004); Accenture: Revenues, Profits Up, Stock Down (Oct 2004); Capgemini: A Takeover Target? (Oct 2004); Sellout of America (Oct 2004); Spy Wars (Sep 2004); Outsourcing Boomerang (Sep 2004); EDS to Cut Up to 20,000 More Jobs (Sep 2004); Capgemini Stock Plummets on Unexpected Loss (Sep 2004); HP Savaged by Wall Street (Aug 2004); Moody's Lowers the Boon on EDS (July 2004); HP: Delivering Value Horizontally (June 2004); Accenture: Revving Up a Notch (June 2004); Beware Your CFO! (May 2004); IBM: Changing of the Guard (May 2004); Capgemini: Texas-size Home Run (May 2004); Following the Money (May 2004); EDS: On a Wink and a Prayer (Apr 2004); HPS Wins by a Nose! (Octathlon 2004); Accenture: Burning the Track (Mar 2004); IGS: "Crown Jewel" Restored? (Mar 2004); HP: Still No Cigar (Feb 2004); Cap Gemini: Another, Smaller Loss (Feb 2004); CSC: Good Quarter Gets Boos (Feb 2004); EDS: "Hot Air Jordan" Flaunts Flop as Feat (Feb 2004); IT Industry: Whither Goeth It? (Jan 2004); Cronyism Is Alive and Well at EDS" (Jan 2004)

![]()

Or just click on  and use appropriate

keywords.

and use appropriate

keywords.

Volume XXI, Annex Bulletin 2005-16 Bob Djurdjevic, Editor 4440 E Camelback Rd #29, Phoenix, Arizona 85018 The copyright-protected information contained in the ANNEX BULLETINS and ANNEX NEWSFLASHES is part of the Comprehensive Market Service (CMS). It is intended for the exclusive use by those who have contracted for the entire CMS service. |

Home | Headlines | Annex Bulletins | Index 2005 | About Founder | Search | Feedback | Clips | Activism | Client quotes | Workshop | Columns | Subscribe