Annex Bulletin 2007-05 February 7, 2007

A partially OPEN client edition

Recent... ![]()

Fujitsu: Sales Up, Profit Down (Analysis of Fujitsu's third quarter fiscal 2007 business results)

IBM Shatters Records (Analysis of IBM's fourth quarter business results)

IT SERVICES

![]()

Updated 2/21/07, 11:0AM EST, adds Market Update

Analysis of EDS' Fourth Quarter Business Results

On Sunny Side of Street

Jordan's Turnaround Finally Getting Traction; Best Quarter Since Early 2002 Lifts Stock

SCOTTSDALE, Feb 7 - Electronic Data Systems (EDS) is on the sunny side of the Street. Its excellent fourth quarter report card, released after the market closed today, helped lift the stock over 4% to $28.18 in after-hours trading, surpassing the 52-week high set in early March of last year.

That's the highest level EDS shares have reached since their precipitous crash in September 2002 (see "EDS Issues Early Warning" and "Wall Street Vultures," Sep 2002). That was the beginning of the end for Dick Brown, the former chairman and CEO. Less than six months later, he was replaced by Michael Jordan (see "EDS CEO Replaced," Mar 2003).

Jordan, 70, who made his claim to fame by masterminding a Westinghouse turnaround in the 1990s, was slow getting the EDS ship to respond. But his efforts are now finally getting traction.

�On balance, this was the strongest quarter EDS has had since I joined the company in 2003,� he said today in a release about the latest EDS results.

Quarterly

Highlights

Indeed, most of the business indicators are up, some in double digits. Fourth quarter adjusted earnings were 47 cents per share, up a whopping 124% from the year before. More importantly for Wall Street investors, they handily beat the average analyst estimates (of 37 cents per share). Which is why the stock rose in response to the news.

Revenues: Fourth quarter revenues were $5.7 billion, up 11%, while organic growth was 7%. For the full year, revenues were $21.3 billion, up 8% from $19.8 billion in 2005, This also means that EDS has reclaimed the No. 2 spot in the global IT services industry, leapfrogging over Fujitsu, its technological partner.

New

Contracts:

EDS signed $7.6 billion in new business during the

quarter, up 43% from a year earlier. Vodafone, the U.S. Department

of Veterans Affairs and the U.K. Ministry of Defense, Kraft Foods and Bank

of America were among the customers that signed bigger deals. For

the full year, the new contract awards amounted to $26.5 billion, the

best annual performance since 2001 (click on thumbnails to enlarge

charts).

New

Contracts:

EDS signed $7.6 billion in new business during the

quarter, up 43% from a year earlier. Vodafone, the U.S. Department

of Veterans Affairs and the U.K. Ministry of Defense, Kraft Foods and Bank

of America were among the customers that signed bigger deals. For

the full year, the new contract awards amounted to $26.5 billion, the

best annual performance since 2001 (click on thumbnails to enlarge

charts).

Despite

a sustained improvement in EDS' new contract

Despite

a sustained improvement in EDS' new contract signings for the third year in a row, the No. 2 IT services company in the

industry continues to be outsold by the No. 1 by a wide margin. In

2006, IBM closed nearly twice as much new business as EDS ($49.3B

vs. $26.5B).

signings for the third year in a row, the No. 2 IT services company in the

industry continues to be outsold by the No. 1 by a wide margin. In

2006, IBM closed nearly twice as much new business as EDS ($49.3B

vs. $26.5B).

Cash Flow:

Full

year

2006 free cash flow was also strong - $887 million, versus $619 million for

the year earlier.

Business

Segment

Analysis

EDS geographic segments turned in a fairly balanced performance in the fourth quarter. All segment comparisons that follow are in constant currency. The continued weakness of the U.S. dollar relative to the euro generally boosted the results in Europe.

Americas:

Fourth quarter revenue was $2.58 billion, up 6%t compared to the

prior-year period. Operating

profit was $506 million, up 20% from $421 million in 4Q05.

Europe:

Fourth

quarter revenue was $1.71 billion, up 6 percent compared to the prior-year period, and up 10 percent on an organic basis (excludes

impact of Global Field Services divestiture). Operating profit (excluding

loss from Global Field Services divestiture) was $310 million, up 24

percent from $251 million in the prior-year period, due to improved

contract execution.

to the prior-year period, and up 10 percent on an organic basis (excludes

impact of Global Field Services divestiture). Operating profit (excluding

loss from Global Field Services divestiture) was $310 million, up 24

percent from $251 million in the prior-year period, due to improved

contract execution.

Asia/Pacific:

Fourth

quarter revenue was $410 million, up 19% compared to the prior-year period

primarily due to MphasiS revenues (a 2006 acquisition of a majority

position [77%] in an Indian IT services company). Operating profit

soared to $52 million, up 176% from $19 million in the 2006.

U.S.

Government:

Fourth quarter revenue was $825 million, up 10% compared to the 4Q05.

Operating profit was $191 million, up 58% from $121 million.

Revenue and operating profit increases were driven in large part by the

improved performance of the Navy Marine Corps Intranet contract.

Industries: Meanwhile, government and retail were the best performing vertical segments for EDS in the fourth quarter. They were up 15% and 32% respectively. Government now accounts for the largest slice of the EDS industry pie (35%), followed by finance & insurance (20%), and manufacturing (16%).

More, Bigger Acquisitions to Follow?

Considering the new EDS acquisitiveness exhibited by the MphasiS deal

in 2006, Wall Street analysts questioned Jordan on his acquisition

strategy. At one point, he said that he would consider making an

acquisition with a price tag in excess of $1 billion.

After the conference call, however, the CFO Ron Vargo told Reuters that the company doesn't "have anything lined up."

"It might make sense," Vargo said in an interview, "based on some of the industries where we have strong presence and capabilities."

Those areas include providing information technology services for

companies in the health-care, manufacturing and financial services

industries, he added. The U.S. and UK governments, for example, are also major clients,

Vargo said.

If

EDS were to pursue additional acquisitions in the vertical industries it

serves, this would reinforce a trend that was already discernible in the

fourth quarter. As can be seen from the two thumbnail charts

(revenue - above right and bookings - left), sales of new applications

contracts have already outpaced the revenue growth of the current

ones. Which bodes well for this horizontal sub-segment in the

future.

If

EDS were to pursue additional acquisitions in the vertical industries it

serves, this would reinforce a trend that was already discernible in the

fourth quarter. As can be seen from the two thumbnail charts

(revenue - above right and bookings - left), sales of new applications

contracts have already outpaced the revenue growth of the current

ones. Which bodes well for this horizontal sub-segment in the

future.

Outlook

Speaking

of the future, EDS

said it expects revenues of $22.0

billion to $22.5 billion this year. Free Cash Flow should be in the

$1.0 billion to $1.1 billion range (vs. $887 in 2006). And with much

of the big cost cutting and offshoring behind it, EDS can look forward to

improving profitability, too (click on thumbnail to view the gross profit chart). The company

forecast an adjusted

EPS of $1.60, a big jump from the $0.96 EDS earned in 2006.

(click on thumbnail to view the gross profit chart). The company

forecast an adjusted

EPS of $1.60, a big jump from the $0.96 EDS earned in 2006.

So

with all EDS lines finally pointing upward (click on left  thumbnail

to enlarge revenue chart), including the long beleaguered

U.S. Navy contract, one can concur with CEO Jordan's assessment that the

turnaround is now complete. He is now preparing to launch "Act

2," he told the analysts during the post-earnings

teleconference. He promised to provide details on that

plan at a company Feb. 20 analyst meeting in New York.

thumbnail

to enlarge revenue chart), including the long beleaguered

U.S. Navy contract, one can concur with CEO Jordan's assessment that the

turnaround is now complete. He is now preparing to launch "Act

2," he told the analysts during the post-earnings

teleconference. He promised to provide details on that

plan at a company Feb. 20 analyst meeting in New York.

Judging by the positive market reaction in after-hours trading, however, looks like Jordan has already secured the investors' benefit of the doubt.

|

Click here for detailed 2007 EDS forecast (Annex clients only) |

Happy bargain hunting!

Bob Djurdjevic

![]() Click

here for PDF (print) version

Click

here for PDF (print) version

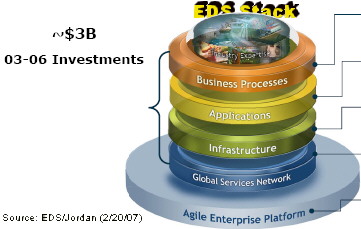

EDS Turnaround, Act II: Climbing Up the Stack

Company to Pursue "Higher Margin, Higher Growth" Opportunities

NEW YORK, Feb 21 - There

were no theatrics when EDS executives presented yesterday their plan for

"Recovery, Act II,"  at

the charming old Hudson Theater on Broadway (click

at

the charming old Hudson Theater on Broadway (click on photo thumbnails to enlarge). EDS chairman and CEO, Michael

Jordan, said the company would "climb up the stack" to

"drive higher margin, higher growth market segments."

on photo thumbnails to enlarge). EDS chairman and CEO, Michael

Jordan, said the company would "climb up the stack" to

"drive higher margin, higher growth market segments."

And what stack is that? The industry solutions stack, as depicted above in an excerpt from a slide the EDS CEO and other executives used during their presentations. The company will endeavor to provide more industry based solutions, either by developing them itself, or by using its formidable stash of cash to acquire such capabilities (also see "More, Bigger Acquisitions," above).

A "Deja Vu," "Back to the Future" Trip?

Funny

how the above sounded to us as a "deja vu" strategy, a trip

"back to the future;" a trek to a long gone and almost forgotten

"future." Back in 1990, we urged IBM and EDS to climb up a

similar stack (see "Industry

Stratification

Trend," Mar 1990 and the related chart -

right). We called it the global solutions providers

"general contractors" and said they would occupy the "top of the industry food

chain."

trek to a long gone and almost forgotten

"future." Back in 1990, we urged IBM and EDS to climb up a

similar stack (see "Industry

Stratification

Trend," Mar 1990 and the related chart -

right). We called it the global solutions providers

"general contractors" and said they would occupy the "top of the industry food

chain."

At the time, EDS was organized by industry. It was split up into three dozen semi-autonomous units which Les Alberthal and Gary Fernandes, the two top EDS executives at the time, called SBUs (Strategic Business Units). The SBUs were all aligned with respective industries they served. It was the first time a major IT company had organized itself that way.

We hailed the approach at the time as innovative, called it the "amoeba syndrome" in a 1993 Annex Bulletin (93-16, 3/18/93), and pointed it out in many of our subsequent reports, presentations and media quotes. By 1994, IBM had also adopted the industry orientation in its services organization. And now, we were hearing it again from EDS as a "new" strategy; a key part of "EDS Recovery, Act II."

Looking around the room, I realized that a vast majority of the audience were probably in high school at the time, and would not have had a clue about the SBUs or the industry stratification trend. They looked perfectly content to accept EDS' "new" strategy as such.

The only person in the room who might have understood my thoughts were he able to read them, was Jeff Heller, EDS' vice chairman. Heller retired from EDS in 2002, but was brought back a year later by the Board as President and COO, along with Jordan, the CEO. At the time, the company's Navy megadeal sprung a huge leak, and Heller was put in charge of plugging it. Always a no nonsense, straight shooting executive who goes back to the early Ross Perot days at EDS, that's exactly what Heller proceeded to do. He plugged the gusher.

Last

year, the Navy contract made money for EDS for the first time in its

six-year history (see above). The successful turnaround established

the company as a pre-eminent defense contractor. Which, in turn,

helped it land two other multi-billion dollar deals with the U.K. Defense Ministry.

As a result, the government sector is now EDS' biggest industry segment

(see the chart).

In a one-on-one conversation before the start of the New York conference, Heller modestly waived off the compliment about the Navy contract turnaround.

"Oh, that's still a wily deal," he said, like a good coach reminding his team not to relax after a winning streak as there's still a long season ahead.

"That may be, but at least you've got the Navy now sailing in the right direction," this writer replied. :-)

Meanwhile, back to "EDS Turnaround, Act II," a series of presentations by top EDS executives who followed Jordan on the Hudson theater stage did not provide any new concrete information about how the company intended to move up the stack, as its CEO said. So we focused during the final Q&A on the unsaid.

Contradictory Goals: No Mention of SMB, Fujitsu

Striving for high margins and high growth are often contradictory goals in the IT services game, we pointed out during the Q&A. Megadeals are a case in point. Winning them is a boost to growth but not necessarily one to the bottom line, as EDS found out the hard way.

"The only place where we have seen both is in the SMB market," this writer said. "And yet we have not heard a word about SMB in any of your presentations today." So we asked Jordan if he would care to comment about that omission.

The EDS CEO acknowledged

that the SMB marketplace does have those attractive characteristics.

And he pointed to some partnerships the company is pursuing in this

area. But Jordan felt the company's bread and butter business was

with the top 2,000 global corporations.

characteristics.

And he pointed to some partnerships the company is pursuing in this

area. But Jordan felt the company's bread and butter business was

with the top 2,000 global corporations.

Another thing that can help improve the profit margins is lower costs. Back in 2005, EDS and Fujitsu announced a strategic technological partnership that this writer thought was supposed to help EDS lower the cost of hardware it installs for clients.

"We have heard a lot of talk about 'best shore' (an EDS euphemism for offshore cost savings) this morning, but again not a word about the Fujitsu partnership," this writer said. "Why not?"

Jordan's answer made it clear that we had overestimated the scope and the importance of that relationship. The partnership seems limited to some Unix servers and Fujitsu mainframes.

"We'd love the IBM mainframe monopoly get chopped up a bit," said Jordan.

Alas, that does not appear to be in the cards any time soon. As we have seen from IBM's fourth quarter report card, the Big Blue mainframes are having a banner revival."

Beating the Competition

Ron Rittenmeyer, EDS' new COO,

also talked a lot about the company's past successes, especially in 2006. He flashed a slide (right) that

showed how successful EDS has been against its four major competitions -

IBM Global Services, Accenture, HP Services and CSC.

successes, especially in 2006. He flashed a slide (right) that

showed how successful EDS has been against its four major competitions -

IBM Global Services, Accenture, HP Services and CSC.

We asked executives of the EDS competitors to comment about these Rittenmeyer claims, but have not received their replies before going to press with this report.

Pointing out a 52% reduction in "severity 1" outages, Rittenmeyer concluded, "it's the quality emphasis that changes us from an outsourcer to an innovator."

Meanwhile, Mike Boustridge, EDS' head of global sales and marketing, and Paul Currie, executive VP in charge of corporate strategy and business developmen, did provide some interesting financial data about the future acquisitions. One of their charts showed that EDS has assembled a formidable war chest for such investments....

... $3 billion, $4 billion and $5 billion of cumulative funding capacity in the next three years. Which means that even bigger acquisitions (of $1 billion or more) are not out of the question, as Ron Vargo, the CFO, said two weeks ago (see above).

"Now it's time to enhance our growth," summed up Jordan the CEO in his closing remarks.

Summary

Given that there was not much new that we learned about EDS' new strategy after the half-day session with its top brass, does that mean that "EDS Turnaround, Act II" has no legs?

Not at all. Plagiarism is a form of flattery, they say. And what better way to plagiarize than to emulate one's own past successes. An industry and global solutions orientation was the right thing way to go 17 years ago. It still is. It's just that EDS leaders lost sight of that idea during the Dick Brown era when they focused on horizontal activities.

Now that the company is

going "back to the future," it is also returning to its own (successful) past. And that's a good thing, in our books.

(successful) past. And that's a good thing, in our books.

It seems the stock market investors liked it, too. EDS shares rose slightly in the aftermath of the New York meeting (see the right chart).

Additional Photo Gallery

Click on photo thumbnails to enlarge...

For additional Annex Research reports, check out... Annex

Bulletin Index 2007 (including all prior years' indexes) Or just click on SEARCH and use "company or topic name" keywords. Volume XXIII, Annex Bulletin

2007-05 Bob Djurdjevic, Editor 8183 E Mountain Spring Rd, Scottsdale, Arizona 85255 The copyright-protected information contained in the ANNEX BULLETINS is part of the Comprehensive Market Service (CMS).

It is intended for the exclusive use

by those who have contracted for the entire CMS service. ![]()

![]()

February 7, 2007

(c) Copyright 2007 by Annex Research, Inc. All rights reserved.

e-mail: annex@djurdjevic.com

Tel/Fax: +1-602-824-8111

Home | Headlines | Annex Bulletins | Index 1993-2007 | Special Reports | About Founder | Search | Feedback | Clips | Activism | Client quotes | Speeches | Columns | Subscribe

Also

check out...![]()

IBM Shatters Records (Analysis of IBM's fourth quarter business results)

IBM Stock Passes Century Mark (Analysis of Big Blue's Stock Performance)

Happy Days Are Here Again (Analysis of Top 20 IT leaders' latest stock market and business performances)

"Excellenture" Excels Again (Analysis of Accenture's first quarter fiscal 2007 business results) [Annex clients click here]

Hedging the Bets (Analysis of latest institutional shareholdings of leading IT companies: IBM, HP, Accenture, EDS, CSC, BearingPoint, ACS, Perot ) [Annex clients click here]

Globalization Accelerates (Analysis of United Nation's annual survey of global investments)

IBM: A $125-Stock? (An update to "From Small Acorns Mighty Oaks Grow")

Capgemini: Longest Sustained Stock Price Rise (An update to "By Leaps and Bounds")

HP: New King of the Hill (Analysis of HP's fourth quarter business results)

IBM: From Little Acorns Mighty Oaks Grow (Analysis of IBM's "State of the Union")

Capgemini: By Leaps and Bounds (Analysis of Capgemini's preliminary third quarter business results)

Fujitsu: Good Performance Gets Better, More Global (Analysis of Fujitsu's first half FY2007 business results)

IBM: A Slam Dunk Quarter (Analysis of IBM third quarter business results)

Accenture's Emphatic Year-end Accents (Analysis of Accenture's fourth quarter results) [Annex clients click here]

IBM: Services in a Box (Analysis of IBM Global Services' Ground-shifting Announcements)

Strong Comeback by IT Stocks in Third Quarter (Analysis of top 20 IT companies' market and business trends)

Stock Buybacks: A Fading Fad (Dell, erstwhile "King of Fluff," suspends its stock buybacks)

Capgemini: Growth Continues (Revenues, net profit up in double digits, margins also improve)

HP Firing on All Cylinders (Stock sets new multi-year record following excellent third fiscal quarter results) [Annex clients click here]

Power of Manpower (While others move to India, Russia... AMD invests in New York, hailing "phenomenal" quality of its labor force)

Ebb Tide Lowers Most Boats (Analysis of EDS' and CSC's latest quarterly results)

IBM Stock Grossly Undervalued? (Analysis of stock market valuations of IBM and its major competitors) [adds latest Fujitsu, Capgemini results]

IBM vs. HP: A Tale of Two Blues (Both companies are doing well in business, but only HP is favored by Wall Street; Big Blue trying to change that now with its new "India Opus") [Annex clients click here]

Go East, Young Man! (A speech delivered in St. Petersburg, Russia, May 25, 2006; click here for slides)

IBM 5-Yr Forecast: Steady As She Goes (Emphasis on quality continued) [Annex clients click here]

Octathlon 2006: Accenture Again Wins "Gold!" (HP gets "Silver," IBM "bronze") [Annex clients click here]

![]()