Annex Bulletin 2010-13 October 1, 2010

A partially OPEN edition

Recent... ![]()

Poised for Solid Growth Again - Analysis of Accenture's fourth quarter results

"Black Continent:" Biggest "White Space" Left - Analysis of IBM-Bharti deal

IT SERVICES

Updated 10/03/10, 4:30PM HIT, adds CEO's comment on SMB, emerging markets

Analysis of Accenture's Fourth Quarter and Full Fiscal Year 2010 Results

Poised for Solid Growth Again

Strong Finish in FY2010 Heralds Bullish Outlook for Next Year, But Aggressive Expansion May Threaten Quality

HAIKU, Maui, Oct 1 – Recession? Retrenching? Cutbacks? Not at Accenture. On the contrary. Expansion is the name of the game at the IT services industry's third largest company. Accenture has just reported strong fourth quarter fiscal 2010 results, has hired enough new employees to populate a nice size town, and has said the business is poised for solid growth again.

"If you look at confidence of executives in their business, people have pretty much run as long as they can without making major investments," said Bill Green, Accenture's CEO, during a post-earnings teleconference with analysts. "And so we think that 2011 is going to be fairly robust in terms of business spending on important initiatives."

If that were to happen,

Accenture's revenue chart may resemble the shape of the left half of the famous Picacho Peak in Arizona (Picacho means a Coyote in

Spanish). After two years of decline and stagnation, the Coyote is

again raising its head and howling to the moon. But the left image is

only a half of the Picacho Peak. You can see the full image on the

right.

left half of the famous Picacho Peak in Arizona (Picacho means a Coyote in

Spanish). After two years of decline and stagnation, the Coyote is

again raising its head and howling to the moon. But the left image is

only a half of the Picacho Peak. You can see the full image on the

right.

No, we are not trying to imply that a precipitous decline will follow a calamitous rise. But there are risks associated with rapid expansions, as you will see in this story.

![]()

Meanwhile, Accenture's fourth quarter revenues rose 5% in U.S. dollars to $5.42 billion (up 8% in local currency), while net earnings surged 67% to $504 million. New bookings were also strong at $6.5 billion, a total of $25 billion for the full year.

The markets liked what they heard from Accenture on Thursday night. The stock jumped nearly five points on Friday. IBM shares also rose buoyed by Accenture executives' bullish comments. IBM is due to report its third quarter results later this month. But Accenture's optimism was not enough to offset the cold reception that the new HP CEO, Leo Apotheker, received on Wall Street. HP shares dropped on the news despite a generally strong stock market day (see above charts).

Putting Its Money Where Its Mouth Is

How many times have you heard some company executives spout off about how great their business is only to lay a bunch of people off in the coming months or years? Not walking its talk has become almost a rule on perverted Wall Street.

Well, that's clearly not the case with Accenture. There is no question that the company is bullish about its future again. And not just in words. For, words are cheap. The IT services industry's third largest IT firm is putting its money where its executives mouths are.

"We hired roughly about 64,000 people this past year, and we see 2011 shaping up to be similar," said Pam Craig, Accenture's CFO, during the analyst teleconference.

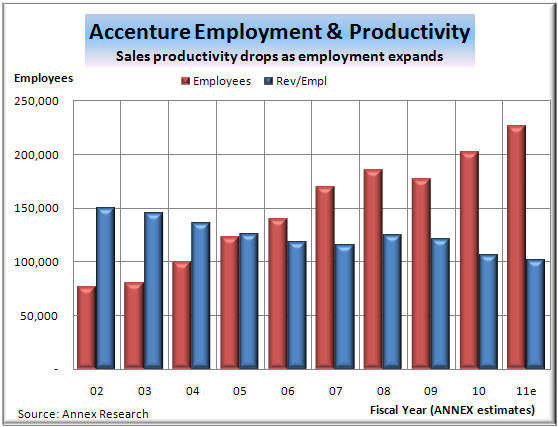

The 2010 hiring spree boosted Accenture's global payroll by 14% to over 200,000 employees. And if its 2011 expansion plan comes true, the company will have grown its employment by about 27% in just two years.

So nobody can accuse Accenture of not putting its money where its mouth is. But there is a price for such a massive expansion. First, in lower sales productivity. Second, in potential quality erosion.

As you can see from the above chart, the higher the employment, the lower sales productivity has been in the last decade. That's because the rate of hiring expansion has exceeded that of the revenue growth.

But that's only a part of the price one has to pay for being aggressive. The second part may be even more troubling...

Quantity over Quality?

"Wait a minute, wait a minute," as Danny DeVito might have famously uttered as one of his American-Italian characters. "Where do you round up 132,000 people in a such hurry?"

Well, probably not in North Dakota or Wyoming. You find them where there are the most people... in places like India, the Philippines, Eastern Europe, Latin America...

Asked by an analyst if most of the new hires were offshore, Craig, the CFO, confirmed that, "yes, the majority were there, but we did hire pretty nearly everywhere, including a lot in the US."

The Accenture executive didn't elaborate on what "a lot" meant. And nobody pressed her to quantify such a vague comment.

The question that we pondered, however, was, "where do you find 132,000 GOOD people in such a hurry?"

And the answer is - you don't. So we wonder if Accenture is now putting quantity ahead of quality? For years, the company has been held up even by its competitors as a model of a high quality operation. A major reason for that has been its winning culture, which was protected and applied consistently across the company.

Adding 132,000 people over a two-year period is equivalent of having several complete blood transfusions. Take into account about a 15% to 17% annual attrition, and you end up with a new body and a different culture under the same name.

So what, you say? Bigger is better. Not necessarily. Not in the services game. That's where quality is not only everything; it is the only thing that will assure a contract renewal.

The main danger of such an aggressive expansion is that the quality of service may suffer. Preventing that is also the main challenge the Accenture leaders face. No business automation aids we have seen so far in the marketplace can offset the value of a competent person. And putting 132,000 rookies on the line has got to dilute the quality of the entire team. There's just no two ways around it.

It is interesting that no analyst broached that subject during in the Q&A session at the post-earnings teleconference. As usual, Wall Street seems ready to lap up any sap companies dish out. We cannot help but wonder, however, how many Accenture clients may be also asking the same question: Is their vendor of choice now putting quantity over quality?

"Robust Demand" Expected in 2011 from New Business Functions

Meanwhile, one reason Accenture is so bullish about the future is that they see the renewed demand for their services as self-generated. Which means it is a repeatable and a dependable basis for future plans and forecasts.

"A lot of this demand we went and created," Green, the CEO, told the analysts. "And we created it by having very specific offerings that deal with specific problems in specific industries."

"As the economy does come back... it's coming back looking different," he continued. "And that's what's driving the demand: business model changes, and delivery channel changes and things like that."

"I think we're going to see consistent budgets for the traditional work, but we're going to see budgets that don't necessarily come out of IT but come out of marketing or engineering or manufacturing to do the new things, to sort of reinvent delivery models, production models and operating models."

Asked in a subsequent email how important the SMB (small and medium size business) and the emerging markets are in Accenture's scheme of things, Green replied that, "SMB is not a big swinger for us. Emerging markets is, and the growth rate is very high but on a smaller base."

So while other vendors, like IBM and HP, are focusing on expanding their businesses to Africa, China, etc., Accenture is trying to milk the old cow - developed markets - using new techniques.

"I insist (on) two things," Green continued. "That we never lose our ability to innovate or to grow organically in the most developed and penetrated markets… (where) we still have huge headroom. We reinvent in the developed markets to be most relevant. If you do not do that, then you have to head for the developing."

In other words, developed markets are still Accenture's Plan A. Which makes sense since that's where most of the money still is. Emerging markets are a Plan B.

No wonder, therefore, that even in places where other vendors are reporting sluggish demand, such as in Europe, for example, Accenture's creativity seems to have found a way to unlock the client's treasure troves.

"We've been pleasantly surprised by the demand in Europe," said Green during the teleconference. "Every day you read the paper, you see something and you start to worry. But frankly, the big companies operate on a Pan-European and on a global stage. Elements of their business are doing exceptionally well. People might be a little slow on the hiring, but they're not slow on the capital expenditures. I mean, people are investing in their business... We feel a lot better about Europe than what you read in the newspaper."

Indeed, Accenture's fourth quarter results in Europe bear out this assessment. Business was up 6% in local currencies on the Old Continent even though European revenues declined 3% as reported in U.S. dollars (to $2.2 billion).

In the Americas, Accenture experienced double digit growth in both U.S. dollars and local currency. Fourth quarter revenues surged 11% to $2.5 billion (up 10% in local currency).

Business volumes were also robust in Asia/Pacific. They were up 13% to $688 million (up 7% in local currency).

Business Segment Highlights

Among Accenture's two horizontal segments, Consulting net revenues were $3.1 billion, an increase of 6% in U.S. dollars and 9% in local currency, while Outsourcing net revenues rose 4% in U.S. dollars to $2.33 billion (up 7% in local currency).

Consulting new bookings were $3.5 billion, while Outsourcing contributed $3.0 billion to the fourth-quarter new contracts. For the full fiscal year, that adds up to $25 billion in new bookings. Which is an improvement over last year's total ($23.9 billion). But Accenture's book-to-bill ratio is still way down compared to what it was six years ago (left chart).

In terms of the vertical (industry) segments, all Accenture's operating groups showed growth in the fourth quarter with the exception of Health & Public Service. Here are the highlights:

- Communications & High Tech: $1,164 million, compared with $1,118 million for the fourth quarter of fiscal 2009, an increase of 4 percent in U.S. dollars and 7 percent in local currency.

- Financial Services: $1,115 million, compared with $1,017 million for the fourth quarter of fiscal quarter of fiscal 2009, an increase of 4 percent in U.S. dollars and 7 percent in local currency.

- Financial Services: $1,115 million, compared with $1,017 million for the fourth quarter of fiscal 2009, an increase of 10 percent in U.S. dollars and 14 percent in local currency.

- Health & Public Service: $856 million, compared with $941 million* for the fourth quarter of fiscal 2009, a decrease of 9 percent in U.S. dollars and 8 percent in local currency.

- Products: $1,268 million, compared with $1,122 million* for the fourth quarter of fiscal 2009, an increase of 13 percent in U.S. dollars and 16 percent in local currency.

- Resources: $1,014 million, compared with $943 million for the fourth quarter of fiscal 2009, an increase of 8 percent in U.S. dollars and 9 percent in local currency.

Summary and Outlook

There is no question that Accenture is bullish about its future and that it's putting its money where its mouth is. For fiscal 2011, the company expects net revenue growth to be in the range of 7% to 10% in local currency, and the EPS growth in the range of 13% to 16% to $3.00-$3.08 per share. That's an increase from the range of 12% to 15% the company had previously forecast.

Accenture expects operating margin for the full fiscal year to be in the range of 13.6% to 13.7%. In the just finished FY 2010, the operating margin was 13.5%.

The company expects operating cash flow to be $2.7 billion to $2.9 billion; and free cash flow to be in the range of $2.4 billion to $2.6 billion.

Accenture is targeting new bookings for fiscal 2011 in the range of $25 billion to $28 billion. In the just finished FY 2010, they were $25 billion.

No wonder, therefore, that the Accenture stock surged nearly five points on the heels of its fourth quarter results and such bullish forecast. Our only question is - at what price to quality of services will such an impressive expansion take place?

Bob Djurdjevic

![]() Click

here for PDF (print) version

Click

here for PDF (print) version

![]()

Or just click on SEARCH and use "company or topic name" keywords.

Volume XXVI, Annex Bulletin 2010-13 Bob Djurdjevic, Editor

(c) Copyright 2010 by Annex Research,

Inc. All rights reserved. |

Home | Headlines | Annex Bulletins | Index 1993-2010 | Special Reports | About Founder | Search | Feedback | Clips | Activism | Client quotes | Speeches | Columns | Subscribe

HP: "Winner" in Game of Chicken - Analysis of HP's bid for 3Par

Do As I Say Not As I Do - Analysis of HP CEO Mark Hurd's demise

A Mixed Bag of Goodies - Analysis of IBM second quarter business results

Big Blue Rains Honey on Wall Street - Analysis of IBM 2Q10 business results

As Good As It Gets Still Not Good Enough - IBM 1Q10 results analysis

Between Rock and Hard Place - Analysis of PC users' current choices

Steady, As She Goes - Update to 5-yr forecast for IBM

HP. Capgemini Send Mixed Signals - Analysis of latest quarterly business results

IBM Delivers... - Analysis of IBM's fourth quarter business results

Big Blue Poised for Growth Again - "State of the Union"-type analysis of IBM performance

Rally of Hope over Fact Continues - Analysis of Top IT Cos 2009 performances

Broken Windows, Broken Promises - "State of the Union"-type analysis of current PC/Windows quality

A Shrinking Giant - Analysis of HP's fourth fiscal quarter business results

IBM Stock Takes a Beating (Analysis of IBM's third quarter business results)

Obama's "Don Quixote" Swings and Misses (Analysis of DoJ's latest antitrust investigation of IBM)

Triple Trouble Hits Armonk (Analysis of insider trading charges against a senior IBM executive)

A Rally of Hope over Fact - Analysis of Top 18 IT companies' performances

Tempest in a Tea Pot (Analysis of latest IT services industry M&A's)

Less Than Meets the Eye - Analysis of HP's 3QFY09 results

Big Blue Blows Lid Off Forecasts - Analysis of IBM's 2Q09 results

Apple, Google Lead Comeback - Analysis of Top IT Cos' stock & business performances

Revenues, Earnings Drop - Analysis of Accenture's 3QFY09 business results

IBM Wins the "Gold" - Analysis of IT Services Octathlon 2009 results

Suddenly, All Lines Point South - Analysis of HP's 2Q09 business results

Back on Growth Track - Analysis of IBM Global Services 2008 results

Sometimes Less Is More and Down Is Up - Analysis of IBM's 1Q business results

IBM's Holistic Approach - Treating businesses like living organisms - secret of success

IBM Tries to Pull Dow, HP Up - Big Blue stock up sharply after CFO remarks at investor conf

Hurd's First Stumble - HP's 1Q09 revenues, earnings disappoint Wall Street

Two Thumbs Up for Big Blue - Analysis of IBM 4Q08 business results

Big Blue: All Heart - IBM creating new jobs in American Heartland

When You Catch a Tiger by the Tail... - An editorial about greed & success

Squeezing the Consumer Dry (Greed fueled both bankers & oilmen's try to squeeze blood out of stone - consumer)

The Year of Living Dangerously - Analysis of global investment trends