Annex Newsflash 2005-36 November 17, 2005

A Partially OPEN Client Edition

INDUSTRY TRENDS

Updated 11/17/05, 11:30PM MST (adds Outlook)

Analysis of HP's Fourth Quarter FY05 Business Results

Best Gets Even Better

HP - Already Best Performing Dow Stock in 2005 - Jumps 6% on Better-Than-Expected Earnings, Revenues

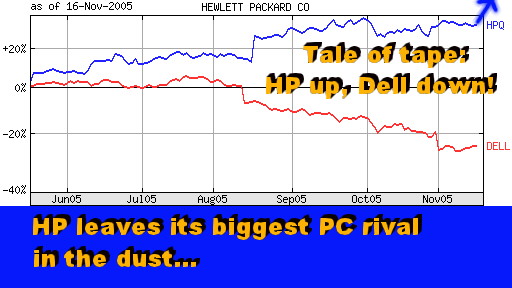

SCOTTSDALE, Nov 17 - Hewlett-Packard (HP), already the best performing Dow Jones stock in 2005, just got even better. The company's shares surged 6% to $30.80 in after-hours trading following the release of its fourth quarter results (for fiscal year 2005, ended Oct 31). That's a new 52-week and multi-year record.

The HP stock had also risen 2.5 points earlier today in regular trading that preceded the earnings release (see the chart).

HP's stock performance over the last six months left its chief hardware rival's in the dust. HP shares have soared by about as much as Dell's have declined (see the chart). This seems to spell the end of an erstwhile Wall Street darling's reign (Dell). But is it a start of another, older tale?

Maybe. For HP, it's a

rags-to-riches story. For Mark Hurd ,

HP's new CEO who engineered this stock market turnaround, it's a quick

gratification for leading his company back to basics.

,

HP's new CEO who engineered this stock market turnaround, it's a quick

gratification for leading his company back to basics.

"We're trying very hard to focus on our core business," said Hurd, who replaced former CEO Carly Fiorina in late March. "We've got some good growth and were prudent with our spending."

That's back to basics: blocking and tackling; followed by some more blocking and tackling...

Nothing fancy, but the results are good. Even better news was that HP's fourth quarter earnings and revenues exceeded Wall Street's expectations. Investors largely shrugged off the $1.1 billion write-off that caused a sharp drop in reported earnings, and focused instead on positive growth outlook and cost cuts.

For the three months ended Oct 31, HP reported net income of $416 million, or 14 cents per share, down from $1.1 billion, or 37 cents per share, in the same period a year ago. Excluding the $1.1 billion charge, however, the HP earnings were $1.5 billion, or 51 cents per share, exceeding Wall Street's expectation of 46 cents per share. And managing expectations is what the stock market has become all about. The new records the HP stock set this evening proved it.

For the full fiscal year 2005, HP reported net income of $4.7 billion, up 16% from last year's, on revenues of $86.7 billion, up 8% from FY04.

Business Segment Analysis

Enterprise Systems.

Enterprise Systems and Storage (ESS) continues to be the HP success story of fiscal year 2005. It is the

company's most improved major business segment. Since the abyss of

the third quarter of FY04, that caused three executive heads to roll (see "HP

Savaged by Wall Street",

Aug 2004), Ann Livermore, the new top ESS executive, has staged a

remarkable turnaround.

to be the HP success story of fiscal year 2005. It is the

company's most improved major business segment. Since the abyss of

the third quarter of FY04, that caused three executive heads to roll (see "HP

Savaged by Wall Street",

Aug 2004), Ann Livermore, the new top ESS executive, has staged a

remarkable turnaround.

In the latest period, ESS revenues grew in double digits, while the unit's operating profit jumped four-fold, from $100 million in the fourth quarter of FY04, to $405 million in the latest period. The ESS operating margin improved from 2.5% to 9.1% in the last 12 months.

For the full year, ESS revenues surged by 11% to $16.7 billion, led by a 24% increase in "industry standard" servers (Intel-based). The "business critical" servers' revenues rose 7%. But perhaps the most impressive fourth quarter growth figures were reported by blade servers (up 65%), by midrange storage arrays (up 44%), and by high-end storage (up 32%).

Annex clients click here for a detailed HP Enterprise Servers & Storage results and valuation

Software.

Software was HP's second most improved unit, recording in the fourth quarter the first profit in its history ($27 million) on a

revenue increase of 11% to $311 billion. For the full year, software

still had an operating loss of $61 million, but that's down from a loss of

$156 million last year.

the fourth quarter the first profit in its history ($27 million) on a

revenue increase of 11% to $311 billion. For the full year, software

still had an operating loss of $61 million, but that's down from a loss of

$156 million last year.

Given the overall size of HP ($87 billion), software still represents one of its most underdeveloped businesses. But at least it is no longer a heavy drain on the company's bottom line. Maybe in FY06, the business will start making money for HP as it does for other software vendors?

Annex clients click here for a detailed HP Software results and valuation

PC. HP's PC unit was another erstwhile beleaguered operation that bounced back nicely in the fourth quarter. Its operating profit soared nearly three-fold (from $77 million to $200 million) on a revenue increase of 9% to $7.1 billion. Notebook revenues jumped by 23%, while desktop business inched up by only 1%

For the full year, HP's PC revenues rose 9%, while its operating profit surged more than three-fold, from $205 million to $661 million. Once again, notebooks led the resurgence with a 16% annual jump, while desktops' revenues rose 2%.

Annex clients click here for a detailed HP PC business results and valuation

Services. HP Services (HPS) also reported revenue growth of 6% in the fourth quarter to $3.9 billion, but its operating profit shrank by 14% to $322 million since 12 months ago. As with several other units, a major reason for the narrower margins were management bonuses paid out at the end of the year. Hurd, the CEO, defended the practice in the post-earnings call with analysts, saying it bolstered morale and helped future performance.

"If you exclude the fourth quarter bonus accrual, operating margins in managed services (outsourcing) and consulting and integration were at their best levels in two and three years, respectively," Hurd told the analysts.

Consulting and integration revenues grew in double digits (up 11%) in the fourth quarter, while outsourcing increased by 9%. The HP maintenance revenues, the biggest HPS segment that accounts for 62% of total revenues, rose by 4%.

For the full year, HPS' revenues grew by 12% to $15.5 billion, while its operating profit slipped by 9% to $1.15 billion. This means that we will probably have a virtual tie for the No. 4 spot in the global IT services market at the end of the year, with Accenture, HPS and CSC all hovering in the $15 billion to $16 billion revenue range (IBM Global Services, Fujitsu and EDS are the top three vendors in terms of revenues). Given the proximity of EDS and Fujitsu's services revenues, we may well have lots of "photo finishes" in our 2006 Global IT Services Octathlon.

Annex clients click here for a detailed HP Services results and valuation

Imaging & Printing. HP's Imaging and Printing Group was again a relative disappointment in the fourth quarter. The company's most profitable unit saw its revenue growth slow to less than 4%, and its operating margins erode from 16.6% to 13.2%. While still enviable in comparison to many other IT vendors' margins, HP's are starting to show the impact of other vendor's competitive pressures, the most notable coming from Dell, a relatively new kid in the printer market.

For the full year, I&P unit's revenues rose by 4% to $25.2 billion, while the operating profits declined by 11% to $3.4 billion. The supplies segment was the most resilient, increasing by 6% to $14 billion. Business printers' revenues also rose by 5% to $6.7 billion, while the consumer business dropped off by 4% to $4.16 billion.

Annex clients click here for a detailed HP Printing & Imaging forecast and valuation

Annex clients click here for a detailed HP Software results and valuation

Annex clients click here for a detailed HP Finance & Investments results and valuation

Things are clearly looking up at HP. Most of its businesses are growing and showing improved profitability. No wonder HP had been the best performer among the Dow Jones stocks even before today's earnings release. You can expect it to break new records tomorrow.

For the full year FY06, HP revenues are expected to be in the range of $89.5 billion to $91.0 billion, the company said. That's a rather conservative forecast, on the low side of Wall Street estimates. Clearly, HP does not want too much euphoria in the stock market at this point, so it's trying to temper future outlook.

Full year earnings per share is expected to be in the range of $1.88 to $1.95, the company said, excluding approximately $0.13 of stock-based compensation expense; or $1.75 to $1.82, including the stock-based compensation. That's about what Wall Street is currently expecting.

So is there still some upside left in the HP stock? Probably, based on the investors' reaction to its latest results. The market seems insatiable. But our analysis of individual businesses that make up the conglomerate that HP is today, shows that the company's current market cap is already about $8.5 billion greater than the some of the parts (see the chart). HP bulls would probably claim synergy as the reason. But the bears may choose to take profits while euphoria pervades opinions.

HP's trailing P/E (price/earnings) ratio of 27.72 (before this evening's surge) towers over IBM's, for example, of 16.84. And IBM is the closest competitor to which one can compare HP in the global IT market. When it comes to forward-looking P/E, however, the two companies are more closely aligned, with HP holding a 15.93 to 15.35 edge over IBM. But this is likely to widen tomorrow, as the stock market puts a higher price tag on better-than-expected HP fourth quarter results.

So yes, maybe there is still some upside left in the HP stock, but not much. That's, of course, if common sense and reason prevail. Alas, they often don't on Wall Street these days, where investment cash flows, not companies business fundamentals, more often than not drive the stock prices.

Annex clients click here for a detailed HP Consolidated FY2005 results and valuation

Happy bargain hunting!

Bob Djurdjevic

For additional Annex Research reports, check out... 2005

IT: HP:

Best Gets Better (Nov 2005); IBM

Hardware Revival (Nov 2005); Tap Dance

Lifts EDS Stock (Nov 2005); Big

Blue Thinks Small Is Big (Oct 2005);

Global

Investments: Yin-Yang Pacific Tsunamis (Oct 2005); IBM:

Springboard Quarter

(Oct 2005); Top

Wall St Firms Bump Up Investments (Oct 2005); Accenture:

A Whopper Quarter

(Oct 2005); Global

Investments: New "Drang Nach Osten" (Sep 2005); HP:

Sweet Turnaround (Aug 2005); Dell

Spooks Street (Aug 2005); EDS Ups Its Forecast

(Aug 2005); Capgemini

Beats Forecast (July 2005); Fujitsu:

Losses Reversed; Forecast Upgraded (July 2005);

IBM:

Polaris Eclipses T-Rex (July 2005);

IBM

Bounces Back

(July 2005); Accenture:

Smashing Records

(July 2005); Merrill's

New Bull (EDS)

(May 2005);

IBM

Trumps Trump

(May 2005);

Tweaking

Big Blue

(May 2005); Hurd's

First RBI (May

2005); Dell

Rings the Bell (May

2005); Stock

Buybacks: The Phantom Is Back (May

2005); EDS Misfiring

on All Cylinders (May

2005);

HP

Surges, Dell Slumps; Lenovo Completes IBM Deal

(May 2005);

![]()

2004 IT: EDS: The Titanium Stock (and other Wall Street tales) (Dec 2004); IBM PC: Good Riddance (Dec 2004); Fujitsu: Recovery Continues (Nov 2004); IBM Server Renaissance (Nov 2004); HP Hits Home Run (Nov 2004); Capgemini: Revenue, Stock Soars (Nov 2004); EDS: Jordan's Swan Song? (Nov 2004); To Russia with Love and $ (Oct 2004); IBM: Slow Quarter No Longer (Oct 2004); Accenture: Revenues, Profits Up, Stock Down (Oct 2004); Capgemini: A Takeover Target? (Oct 2004); Sellout of America (Oct 2004); Spy Wars (Sep 2004); Outsourcing Boomerang (Sep 2004); EDS to Cut Up to 20,000 More Jobs (Sep 2004); Capgemini Stock Plummets on Unexpected Loss (Sep 2004); HP Savaged by Wall Street (Aug 2004); Moody's Lowers the Boon on EDS (July 2004); HP: Delivering Value Horizontally (June 2004); Accenture: Revving Up a Notch (June 2004); Beware Your CFO! (May 2004); IBM: Changing of the Guard (May 2004); Capgemini: Texas-size Home Run (May 2004); Following the Money (May 2004); EDS: On a Wink and a Prayer (Apr 2004); HPS Wins by a Nose! (Octathlon 2004); Accenture: Burning the Track (Mar 2004); IGS: "Crown Jewel" Restored? (Mar 2004); HP: Still No Cigar (Feb 2004); Cap Gemini: Another, Smaller Loss (Feb 2004); CSC: Good Quarter Gets Boos (Feb 2004); EDS: "Hot Air Jordan" Flaunts Flop as Feat (Feb 2004); IT Industry: Whither Goeth It? (Jan 2004); Cronyism Is Alive and Well at EDS" (Jan 2004)

![]()

Or just click on  and use "financial engineering" or similar

keywords.

and use "financial engineering" or similar

keywords.

Volume XXI, Annex Newsflash 2005-36 Bob Djurdjevic, Editor 8183 E Mountain Spring Rd, Scottsdale, Arizona 85255 The copyright-protected information contained in the ANNEX BULLETINS and ANNEX NEWSFLASHES is part of the Comprehensive Market Service (CMS). It is intended for the exclusive use by those who have contracted for the entire CMS service. |

![]()

Home | Headlines | Annex Bulletins | Index 2005 | About Founder | Search | Feedback | Clips | Activism | Client quotes | Workshop | Columns | Subscribe