Annex Bulletin 2007-35 October 12, 2007

A CONFIDENTIAL client edition

Recent... ![]()

Seedlings Sprouting Stronger Limbs - Update to "IBM State of the Union" [Annex clients click here]

An Apple a day keeps bear away (Analysis of Top 20 IT companies' market, business performances )

IBM CORPORATE

![]()

Updated 10/12/07, 4:00PM PDT

Update to Our 2007 "State of the IBM Union" Analysis

Seedlings Sprouting Stronger Limbs

Innovation Drives Growth; Server Brand Convergence Leads to New Sales & Marketing Model

Big "Green" Initiative Played Right into Our 2006 Garden Analogy

SCOTTSDALE, Oct 12 - Nearly one year ago,

we first noted that "From

Little Acorns Mighty Oaks Grow" (see right image). The report

was a part of our fall 2006 analysis of the "State of the IBM Union" and

Big Blue's growth prospects. And we concluded back then that, "as

more Wall Street investors turn their eyes from feeds and speeds to

weeds and seeds, more will recognize the growth

potential of the new seedlings in the Big Blue garden. As they do,

the IBM stock will break out of its multi-year slump and surpass that

two-year record."

Well, the IBM stock has certainly done that. It closed yesterday (Oct 10) at $118.32, up 41% from a year ago, but still a little short of our $125-target price, that we also set last fall. In the process, the Big Blue shares have also outperformed the Dow, of which they are a part, by more than double the rate of growth (see left chart).

Since that time, IBM's "green" initiative (see "The Greening of Big Blue", May 2007 and "The Greening of Big Blue, Part 2," Aug 2007) has played right into our garden analogy from last fall. All we needed to do is change the color of the IBM logo from blue to green. Here's an excerpt:

It used to be a business of speeds and feeds. Now it's more about weeds

and seeds. Running a successful IT business these days is not unlike caring for a beautiful garden. It takes a lot of TLC (tender loving care) and creativity. And back-breaking work... planting the seeds for future growth; nurturing them to seedlings; weeding and pruning the excess, thus shaping the design into a "constant gardener's" vision of beauty.

Sometimes, it can be years before results become discernible. Which takes patience and perseverance. Both are in short supply on Wall Street. But "from little acorns mighty oaks grow." Small seeds sprout into pretty seedlings. As Sam Palmisano's new Big Blue garden is starting to take shape, Wall Street is (finally) taking notice of some seedlings that have grown from seeds planted years ago.

(An excerpt from Annex Bulletin 2006-41, Nov 2007)

So how are the "Big Green" seedlings doing a year later? Are there any new ones that have sprouted since that time? Here's our update to last year's fall "State of the Union" analysis...

IBM "State of the Union" Update

With IBM expected to report its third quarter results next week, we can only use the first half results as the latest indicators. And they were good... very good, in fact. Second quarter revenues were up 9% to $23.8 billion, with IBM's biggest and most profitable business segments growing in double digits. Earnings per share grew even faster, rising 15% from a year ago.

Wall Street also liked it, pushing the

IBM shares to about $115 (see "IBM Beats the Street,"

July 2007). That was only three points below the current

near-record level, but quite a bit above the August chasm caused by the

turbulence in financial cre dit markets. The crisis dragged down most

IT stocks, including IBM's, but did not keep them down, as the subsequent

rally lifted the Big Blue shares to nearly a six-year high ($120, set on Oct

2).

dit markets. The crisis dragged down most

IT stocks, including IBM's, but did not keep them down, as the subsequent

rally lifted the Big Blue shares to nearly a six-year high ($120, set on Oct

2).

We had a chance to look more closely into the Big Green garden last week at an IBM Systems and Technology Group (STG) conference in Stamford, CT. And what we saw was some last year's seedlings getting stronger and sprouting new limbs, and some new ones also jutting out of the mighty oak (right chart).

New

"Go-to-Market" Approach.

One of them was a new "go-to-market"

approach, "a change from a brand-centric to a customer-centric format,"

according to Bill Zeitler (right), who heads up the STG, the $22 billion IBM

unit that encompasses all of its hardware businesses.

New

"Go-to-Market" Approach.

One of them was a new "go-to-market"

approach, "a change from a brand-centric to a customer-centric format,"

according to Bill Zeitler (right), who heads up the STG, the $22 billion IBM

unit that encompasses all of its hardware businesses.

"It's the most significant change in 15 years," echoed Bob Samson, the head of IBM's worldwide hardware sales whose job it was and is to implement the new marketing approach (below left).

He said the company first tested its new sales model in China, and the results were "significantly better" than before.

That's not surprising. It's hard to image how you can lose if you put

your customer first. Perhaps the on ly question is what took IBM so

long?

ly question is what took IBM so

long?

We can recall, for example, the former IBM CEO (twice removed), John Akers, declaring 1987 to be "the year of the customer." Which in turn gave DEC, then the main IBM challenger, a chance to mock Big Blue's sales tactics by running ads saying, "at DEC, every year is the year of the customer" (see Annex Bulletin 87-31, May 1987, and "Akers: The Last Emperor," June 1991).

Samson seemed to anticipate such skepticism by asking the rhetorical question himself. He answered it by saying that, as the growth emphasis shifted this year to the SMB and market-specific solutions markets, and a brand consolidation got underway, it became necessary to change the IBM sales model to reflect the new market realities.

And so the preceding is our graphical presentation of the latest IBM seedling, its new three-pronged sales model. Underpinning all three channels is innovation, some through collaboration with customers, IBM executives said.

"You've got to be a foundry of innovation to help change the world a little," said Samson.

His boss, Zeitler, said at the start of the two-day conference that he had never seen more important technology innovations coming down the chute as what IBM has in the pipeline for the next six months.

Server Brand Convergence. Furthermore, IBM can be

expected to converge of its various server brands (x, i, p and z) into a unified "form factor" (box).

This process has already begun in the midmarket, with the merger of the

high-end of the System i and p server lines announced in late July.

Over time, other brands will foll

various server brands (x, i, p and z) into a unified "form factor" (box).

This process has already begun in the midmarket, with the merger of the

high-end of the System i and p server lines announced in late July.

Over time, other brands will foll ow

suit, including the high end of the the "p" and "z," though you should not

expect that in the near future.

ow

suit, including the high end of the the "p" and "z," though you should not

expect that in the near future.

The ultimate "form factor" in which IBM will deliver its "Big Blue in a

Box" solution to SMB and other customers is BladeCenter S (right).

Initially, it has the "i" and the "x" server blades. But eventually it

will include many others, including the new game blades (Cell

processors),

for example, and even competitors' blades (Dell, HP, etc.), according Marc

Dupaquier (left), the former software executive who took over the new IBM

SMB unit within STG in January of this year (see "IBM

Lowers Center of Gravity," Jan 2007).

processors),

for example, and even competitors' blades (Dell, HP, etc.), according Marc

Dupaquier (left), the former software executive who took over the new IBM

SMB unit within STG in January of this year (see "IBM

Lowers Center of Gravity," Jan 2007).

And IBM will wrap its software and services around the Bladecenter S, as

well as the software of its select partners, and have the package sold at

the low end by existing partners as well as through some new channels, such

as telcos, for example. Dupaquier said IBM has already signed 194 of

348 most popular ISVs (Independent Software Vendors) whose software the "Big

Blue in a Box" will offer (right chart).

So with the server technological convergence, the old IBM brand-based sales and marketing organization is becoming redundant and is being replaced with a new three-pronged model, as Samson pointed out. So that's the ultimate IBM answer to the "why now?"-question.

Large Enterprises. At the high end, for example, where IBM

has a 31% overall market share (41% in servers and 24% in storage),

according to Zeitler, IBM's challenged it so keep the growth going through

new initiatives, such as virtualization and IT optimization, and, of course,

the "greening of IBM" and of the customer data centers.

customer data centers.

Globalization is another driving force behind the resurging mainframe demand, noted Jim Stallings (right), the head of the largest IBM server product line. He cited several customer examples, including Citigroup, for example, which bought 124 companies over the last several years.

All that global churning and consolidation is good for IBM mainframe business. The System z revenues were up for the fifth consecutive quarter, while the overall MIPS shipments were up 45%, the eighth consecutive quarter of growth, Stallings pointed out (also see "IBM Beats the Street," July 18).

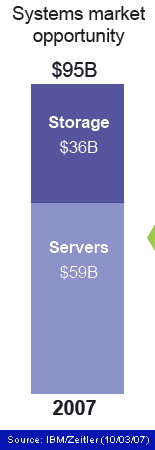

IBM se es

the overall systems market as a $95 billion per year opportunity, about 60%

of it in servers, and the rest in storage (left chart).

es

the overall systems market as a $95 billion per year opportunity, about 60%

of it in servers, and the rest in storage (left chart).

This is a market where power and cooling costs represent a significant

opportunity for savings. And IBM is leading the way by example.

As you you can see from the right chart as well as in "The Greening

of Big Blue, Part 2," (Aug 2007), IBM is going through a massive

consolidation of its IT resources that will result in annual savings of $1.5

billion, according to St eve

Sams, an IBM GTS (Global Technology Services) executive who is spearheading

the effort.

eve

Sams, an IBM GTS (Global Technology Services) executive who is spearheading

the effort.

IBM spends about $500 million annually on energy, and its energy bill is growing at 18% per year, Sams added.

"In most customer sites, we should be able to increase the energy

efficiency by 40% to 50%," he said. Yet "many clients are not (yet)

focuses on energy consumption issues," which is, of course, an opportunity

for a vendor like IBM that thinks it can hel p

customers with such problems.

p

customers with such problems.

IBM's chief hardware technology officer, Dr. Bernie Meyerson, said the power and cooling expenses are growing 800% faster than the customers' spending on servers (right and left charts). So the opportunity for developers and customers to save goes well beyond the traditional ways of scaling and compressing chips, a process that actually increases the heat output.

Custom

Solutions. In what IBM calls the "custom and

embedded solutions" market, one of the new

Custom

Solutions. In what IBM calls the "custom and

embedded solutions" market, one of the new seedlings we analyzed last year, a relatively new opportunity for IBM,

customers are spending about $92 billion per year on various engineering

services, customized systems and chips, according to IBM (right chart).

But since most of the customers consider their own R&D as one of their

"crown jewels," it has been tough for IBM to demonstrate why Big Blue

innovators can do better or more.

seedlings we analyzed last year, a relatively new opportunity for IBM,

customers are spending about $92 billion per year on various engineering

services, customized systems and chips, according to IBM (right chart).

But since most of the customers consider their own R&D as one of their

"crown jewels," it has been tough for IBM to demonstrate why Big Blue

innovators can do better or more.

We s aid

last year that in many respects what Adalio Sanchez (left), the head of IBM

Global Engineering Services (GES), renamed earlier this year from TCS

(Technology Collaboration Services) and his team are trying to do is

reminiscent of the early days of IBM Global Services efforts to promote

outsourcing. Just like now with the R&D prospects, there were a lot of

skeptics among the customer CIOs of the late 1980s and early 1990s that

turning over their data centers to the likes of IBM or EDS or Accenture was

a smart thing to do. It took a few high-profile wins, like Eastman

Kodak or McDonnell Douglas to legitimize the new concept.

aid

last year that in many respects what Adalio Sanchez (left), the head of IBM

Global Engineering Services (GES), renamed earlier this year from TCS

(Technology Collaboration Services) and his team are trying to do is

reminiscent of the early days of IBM Global Services efforts to promote

outsourcing. Just like now with the R&D prospects, there were a lot of

skeptics among the customer CIOs of the late 1980s and early 1990s that

turning over their data centers to the likes of IBM or EDS or Accenture was

a smart thing to do. It took a few high-profile wins, like Eastman

Kodak or McDonnell Douglas to legitimize the new concept.

Well,

the GES team just got their first big milestone win - the Nokia Siemens

Network (NSN). And the key was the customer's perception that IBM

would empower and enhance its own R&D rather than displace it.

Well,

the GES team just got their first big milestone win - the Nokia Siemens

Network (NSN). And the key was the customer's perception that IBM

would empower and enhance its own R&D rather than displace it.

"In order to ensure our world-leading technology capabilities and optimum synergies across the Business Lines, we have decided to strengthen our R&D activities by creating a cost efficient R&D structure." said J�rgen Walter, head of Service Core and Applications at NSN, in a release. "This move provides Nokia Siemens Networks with the flexibility it needs to successfully compete in the market,"

The deal was a part of the $2 billion cost-cutting directive that the Siemens CEO Peter Loescher wants to take out of the NSN cost structure. About 235 NSN engineers from labs in Munich and Berlin will transfer to IBM under the agreement, Sanchez said.

Refusion of Arts & Sciences (revisited). Another IBM

deal in Europe underscored an old industry trend that we first identif ied

in 1994 - a refusion of arts and sciences that the silicon is facilitating.

When the sponsors of the Mare Nostrum data center, the #1 supercomputing

site in Europe, based in Barcelona, Spain, gave IBM the specs as to how they

wanted it built, they insisted it had to be "beautiful" as well as energy

efficient. And that's what they got eventually (right).

ied

in 1994 - a refusion of arts and sciences that the silicon is facilitating.

When the sponsors of the Mare Nostrum data center, the #1 supercomputing

site in Europe, based in Barcelona, Spain, gave IBM the specs as to how they

wanted it built, they insisted it had to be "beautiful" as well as energy

efficient. And that's what they got eventually (right).

"It's the most beautiful site we've ever built," said IBM's Sams. He should know a thing or two about that. Sams and his GTS team have built about 60 new data centers so far, spending an average of only six to eight weeks on each.

Retail Store Solutions. IBM's Retail Store Solutions

is perhaps one of the b est kept secrets inside

the Big Blue. It's what was left over from the PC sale to Lenovo in

2005. Yet it's one of the fastest growing businesses in IBM, and the

only one in which Big Blue actually

est kept secrets inside

the Big Blue. It's what was left over from the PC sale to Lenovo in

2005. Yet it's one of the fastest growing businesses in IBM, and the

only one in which Big Blue actually touches consumer markets directly.

touches consumer markets directly.

Last year, for example, IBM's retail business grew by 21%, with its kiosk

revenues up over 70%, according to Steve Ladwig (left), who heads up this

unit. We estimate that this business will bring contribute $900

million to IBM revenues this year. And IBM has its point-of-sale

(POS) and other servers installed in 65 of the top 100 retailers, Ladwig said.

So Retail Store Solutions is another of Big Blue's seedlings whose growth has been surprisingly strong.

But the real stunner for us was Ladwig's chart (right) that showed that

IBM is the largest POS provider in the business, with more than double the

installed base of the next two vendors combined (NCR and Fujitsu). And

that 94% of retail revenues still comes from the stores, not the web

purchases.

"There has been an unprecedented fragmentation of the consumer markets," he said. So now it takes targeting many more smaller segments for a marketing campaign to work.

Ladwig said that about 40% of the IBM retail business comes from SMB, where his unit now sells through about 2,000 partners now. And once again, IBM's retail SMB delivery is based on the BladeCenter S.

"SMB is a big play for us," he added. "It's growing much faster than the enterprise market."

SMB.

Speaking of SMB, that was one of the promising seedlings

identified in our last

year's "State of the IBM Union" report. And its importance seem to

rise this year when the IBM chairman and CEO said at the Partnerworld

conference in St. Louis in early may that this is the company's most

important growth opportunity (see "IBM:

Lowering Center of Gravity," May 2007).

SMB.

Speaking of SMB, that was one of the promising seedlings

identified in our last

year's "State of the IBM Union" report. And its importance seem to

rise this year when the IBM chairman and CEO said at the Partnerworld

conference in St. Louis in early may that this is the company's most

important growth opportunity (see "IBM:

Lowering Center of Gravity," May 2007).

Alas, its performance so far this year has not exactly lived up to that promise. In the second quarter, for example, SMB revenues were $4.5 billion, up 7% in constant currency over the year before, only slightly higher that the company's average growth of 6% in constant currency during the same period.

Meanwhile, most of the SMB partners through which IBM sells with whom we

talked during our several 'round the world trips in the last year or so

are

growing at 20%, 30% or higher rates, as we also pointed out last year.

So clearly, IBM is not yet fully exploiting this growth opportunity.

are

growing at 20%, 30% or higher rates, as we also pointed out last year.

So clearly, IBM is not yet fully exploiting this growth opportunity.

Furthermore, IBM presenters at a "deep dive" session on SMB got an earful

from consultants and analysts about Big Blue's inconsistent definitions of

SMB market. In many countries, including the U.S., they often includes

some very large companies, only because Big Blue doesn't do much business

with them. That's also something we pointed out in our last year's

report on SMB. So we estimate that IBM's "true SMB" (companies with

1,000 employees or less) will be only about $11 billion in revenues this

year, or 12% of the total.

Which makes this Big Green seedling's growth still more in the "promised land" category than today's reality. Nevertheless, "SMB is the place to be," as we have been heralding for over 10 years now. And the sooner IBM starts to act as an SMB vendor rather than try to retrofit its large enterprise DNA and products into this entrepreneurial environment, the faster its revenues and profits will grow.

Some Strategic Inconsistencies? When Sam Palmisano

said at the Bangalore June 2006 conference for financial analysts that the

company would "exit any busine ss

that is a commodity business," and that IBM would "not rationalize for

synergy" (as Lou Gerstner did by hanging on to the low margin PC business

for so long), we applauded the new IBM strategy. For, we saw it as a

statement about emphasizing "quality over quantity" (left chart). And

that's something that we saw as attractive both from the business

fundamentals, as well as stock market viewpoints.

ss

that is a commodity business," and that IBM would "not rationalize for

synergy" (as Lou Gerstner did by hanging on to the low margin PC business

for so long), we applauded the new IBM strategy. For, we saw it as a

statement about emphasizing "quality over quantity" (left chart). And

that's something that we saw as attractive both from the business

fundamentals, as well as stock market viewpoints.

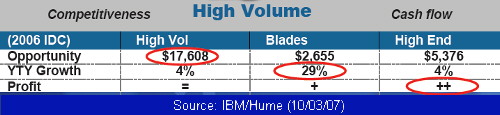

Well, in checking out the various IBM product lines' strategies at the STG Summit last week, we did come across some apparent inconsistencies in the implementation of this IBM chairman's statement of direction.

At the System x breakout session, for example, we learned that the second-largest IBM servers' hardware margins were not as good as that of some of IBM's "traditional servers," according to Rich Hume, who heads up the System x business. No surprise there, considering these servers are based on Intel's chips.

We also learned that the low end of the System x product line accounts

for about half of its revenues, yet has margins that are considerably lower

than those at the high-end of the same product line. Now, that sure

smacked of a commodity-type business to us. So we asked Hume (right)

to explain this apparent inconsistency with IBM chairman's statement of

strategy.

He replied that, "you need the leverage of scale to be able to sustain the high-end business." "Without the high volume (low end) servers, the costs of high-end servers would be much higher."

The last time we checked, this type of an explanation would qualify as cross-subsidization of products. Or "rationalization for synergy," as Palmisano put it in Bangalore when he said that IBM would NOT engage in such practices anymore.

"Customers demand that we deliver top-to-bottom servers," Hume summed it up. And he said that there will be new "specialty form factors" in 2008-2009 in the low end that would help IBM differentiate itself more (presumably leading to higher margins).

But when we asked him if that differentiation might also include some "beautiful servers" at the low end, just like HP or Dell are now doing in consumer markets, or the Mare Nostrum data centerexemplified a refusion of arts and sciences (see above), Hume deferred the question to one of his staffers who seemed clueless about what we were talking about.

Summary: Innovation, Innovation...

Innov ation,

innovation... and then more innovation. That was basically the theme

of Rod Adkins', STG's chief technology officer's (right) summary of IBM's

hardware strategy, as were the earlier presentations by Dr. Meyerson and

Zeitler. The three top IBM hardware executives marshaled out

numerous examples of where IBM's inventions, either in-house or in

collaboration with clients, helped change the world and the shape of the IT

industry.

ation,

innovation... and then more innovation. That was basically the theme

of Rod Adkins', STG's chief technology officer's (right) summary of IBM's

hardware strategy, as were the earlier presentations by Dr. Meyerson and

Zeitler. The three top IBM hardware executives marshaled out

numerous examples of where IBM's inventions, either in-house or in

collaboration with clients, helped change the world and the shape of the IT

industry.

Meyerson, for example, talked about IBM's "holistic" approach to innovation that encompasses everything "from atoms to software." Innovation at Big Blue these days is about "simultaneous optimization of materials, devices, circuits, cores, chips, system architecture, system assets and system software," and, of course, the new big "p" for power. And it is the latter that is turning the IBM's famous blue into green.

Within that holistic approach, there are still pockets of excellence that

are carried out at the old "speeds and feeds" levels. Zeitler, for

example, showed the tremendous expansion of processing power by the Blue

Gene processors at the Argonne National Labs, soon to be dwarfed an order of

magnitude more powerful PERCS processor, based on Power 7, at DARPA (Defense

Advanced Project Research Agency - two above ch arts).

arts).

Adkins also pointed to "hybrid supercomputing" breakthroughs at Los Alamos Labs, where x86, Linux master cluster and a Cell processor cluster are targeting to deliver a 1.4 petaflop peak, 1.0 petaflop sustained performance in project dubbed "Roadrunner" (right).

And so, the beat goes on... faster, smaller, cheaper, cooler is winning the day again, but in a new way, for IBM and its customers. Adkins saw the current period as the "virtualized" era, coming on the heels of "distributed" and "centralized" periods during the first 50 years of the computer industry (left chart). And the STG general managers, whom Zeitler assembled on stage for discussion and a Q&A with analysts and consultants put their own individual spins on the IBM innovation theme.

Overall, IBM seems to be churning out inventions at a rate that even Big Green itself sometimes has trouble consuming, as evident from the IBM-Google announcement this week of "cloud" computing (see "IBM-Google on Cloud Nine?," Oct 2007). Enter the collaboration dimension of innovation. Everybody is welcome to participate. All stand a chance of benefiting from each other's creativity.

"You've got to be a foundry of innovation to help change the world a little," as you saw earlier IBM's Samson declare.

Foundry and an art workshop as well. For, a refusion of arts of sciences is indeed taking place and taking hold of the IT world 13 years after we first discerned it. Leonardo da Vinci would be pleased.

Happy bargain hunting!

Bob Djurdjevic

![]() Click

here for PDF (print) version

Click

here for PDF (print) version

![]()

For additional Annex Research reports, check out... Annex Bulletin Index 2007 (including all prior years' indexes)

![]()

Or just click on SEARCH and use "company or topic name" keywords.

Volume XXIII, Annex

Bulletin 2007-35 Bob Djurdjevic, Editor 8183 E Mountain Spring Rd, Scottsdale, Arizona 85255 The copyright-protected information contained in the ANNEX BULLETINS is part of the Comprehensive Market Service (CMS). It is intended for the exclusive use by those who have contracted for the entire CMS service. |

Home | Headlines | Annex Bulletins | Index 1993-2007 | Special Reports | About Founder | Search | Feedback | Clips | Activism | Client quotes | Speeches | Columns | Subscribe

Also

check out...![]()

Profitable Growth Continues - Analysis of HP's 3Q business results [Annex clients click here]

zAAP-ed by IBM! (Analysis: Mainframe demand benefiting from specialty engines, Java)

Profitable Growth Continues - Analysis of HP's 3Q business results [Annex clients click here]

Sun's Solaris to Shine on IBM's Polaris (IBM to offer Suns OS on its hardware)

The Greening of Big Blue, Part 2 (IBM to save $250M in mainframe consolidation)

IBM Beats the Street (Analysis of IBM 2Q07 business results)

Adios, Microsoft Vista! (How I Failed Twice in Trying to Scale Mt. Vista)

Burning the Track - Firing on all cylinders, Accenture raises forecast [Annex clients click here]

New Broom Sweeps Clean - Analysis of CSC's 4Q07 business results [Annex clients click here]

The Last of the (PC) Mohicans - Analysis of Dell's strategy changes; Linux, Wal-Mart

BRIC by BRIC... to Top Line Growth - Echoes from IBM meeting for fin analysts [Annex clients click here]

Per Ardua Ad Astra - Analysis of HP's 2Q07 business results [Annex clients click here]

The Greening of Big Blue (IBM to spend $1 billion on "going green")

Are We in "Buyback Bubble?" - Analysis of corporate stock buyback trends

IBM: Lowering Center of Gravity (Highlights of Partnerworld 2007, with Detailed Reports for Clients)

Growth Accelerating - Analysis of Capgemini's 1Q07 business results [Annex clients click here]

To Buy (back shares) or Not to Buy? - Analysis of stock buybacks in corporate America

No Surprises in Good Opening Quarter - Analysis of IBM 1Q business results [Annex clients click her

IBM Stock Still Grossly Undervalued (A preview of IBM first quarter business results]

Accenture Beats Forecasts, Again (Analysis of Accenture's 2QFY07 results)

HPS, Capgemini Tie for "Gold" - Results of Octathlon 2007 [Annex clients click here]

The Value of pi (π) - Analysis of IBM System p and System i market and product strategies

IBM Profit to Grow Faster Than Revenue - Update to 5-yr IBM forecast [Annex clients click here]

The (T)ides of March Sink Markets Again - Analysis of global economic & investment trends

IGS: Growth Slows, Profit Surges - Analysis of IGS 2006 business results [Annex clients click here]

HP: Toward New Highs? (Excerpts from analysis of HP's 1Q07 business results) [Annex clients click here]

Capgemini Caps Great Year, Saves Best for Last (Analysis of Capgemini's fourth quarter business results)

EDS: On Sunny Side of Street (Analysis of EDS' fourth quarter business results)

CSC: Where Less Seems More (Analysis of CSC's third quarter fiscal 2007 business results)

Fujitsu: Sales Up, Profit Down (Analysis of Fujitsu's third quarter fiscal 2007 business results)

IBM Shatters Records (Analysis of IBM's fourth quarter business results)

IBM Stock Passes Century Mark (Analysis of Big Blue's Stock Performance)

Happy Days Are Here Again (Analysis of Top 20 IT leaders' latest stock market and business performances)

"Excellenture" Excels Again (Analysis of Accenture's first quarter fiscal 2007 business results) [Annex clients click here]

Hedging the Bets (Analysis of latest institutional shareholdings of leading IT companies: IBM, HP, Accenture, EDS, CSC, BearingPoint, ACS, Perot ) [Annex clients click here]

Globalization Accelerates (Analysis of United Nation's annual survey of global investments)

IBM: A $125-Stock? (An update to "From Small Acorns Mighty Oaks Grow")

Capgemini: Longest Sustained Stock Price Rise (An update to "By Leaps and Bounds")

HP: New King of the Hill (Analysis of HP's fourth quarter business results)

IBM: From Little Acorns Mighty Oaks Grow (Analysis of IBM's "State of the Union")

Capgemini: By Leaps and Bounds (Analysis of Capgemini's preliminary third quarter business results)

Fujitsu: Good Performance Gets Better, More Global (Analysis of Fujitsu's first half FY2007 business results)

IBM: A Slam Dunk Quarter (Analysis of IBM third quarter business results)

Accenture's Emphatic Year-end Accents (Analysis of Accenture's fourth quarter results) [Annex clients click here]

IBM: Services in a Box (Analysis of IBM Global Services' Ground-shifting Announcements)

Strong Comeback by IT Stocks in Third Quarter (Analysis of top 20 IT companies' market and business trends)

Stock Buybacks: A Fading Fad (Dell, erstwhile "King of Fluff," suspends its stock buybacks)

Capgemini: Growth Continues (Revenues, net profit up in double digits, margins also improve)

HP Firing on All Cylinders (Stock sets new multi-year record following excellent third fiscal quarter results) [Annex clients click here]

Power of Manpower (While others move to India, Russia... AMD invests in New York, hailing "phenomenal" quality of its labor force)

Ebb Tide Lowers Most Boats (Analysis of EDS' and CSC's latest quarterly results)

IBM Stock Grossly Undervalued? (Analysis of stock market valuations of IBM and its major competitors) [adds latest Fujitsu, Capgemini results]

IBM vs. HP: A Tale of Two Blues (Both companies are doing well in business, but only HP is favored by Wall Street; Big Blue trying to change that now with its new "India Opus") [Annex clients click here]

Go East, Young Man! (A speech delivered in St. Petersburg, Russia, May 25, 2006; click here for slides)

IBM 5-Yr Forecast: Steady As She Goes (Emphasis on quality continued) [Annex clients click here]

Octathlon 2006: Accenture Again Wins "Gold!" (HP gets "Silver," IBM "bronze") [Annex clients click here]

![]()